24 Apr 24 | Deals Done Waverley House suite let to Traders Connect App on a new five-year lease. Read more

23 Apr 24 | Commercial Crondall Place at Coxbridge Business Park, Farnham acquired by owner-occupier business. Read more

22 Apr 24 | Deals Done Martletts Corner, in Rudgwick in West Sussex acquired by private investor. Read more

09 Apr 24 | Deals Done Private investor secures retail property letting in Lightwater, Surrey Read more

08 Apr 24 | Company News Curchod & Co tops Surrey Commercial Property Market for third consecutive year Read more

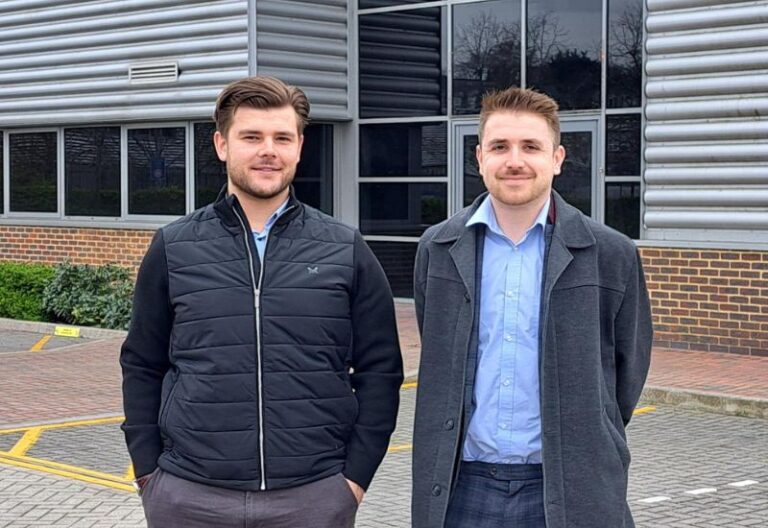

03 Apr 24 | Company News Curchod & Co elevates Tom Nurton and Alex Blown to Associate Partners Read more

06 Mar 24 | Deals Done Lark London takes an assignment of a High Street retail property in Weybridge Read more